Airtel Mobile Commerce Uganda Limited, reported another hack in November 2022 where hackers made off with shs 8bn after accessing accounts of 1,840 users using the website of a local betting platform, as revealed by Daily Monitor. This is just one of the series of hacks that have plagued Mobile Money in Uganda. In 2020, hackers broke into the systems of Pegasus Technologies, the aggregators of both MTN Mobile Money and Airtel Money as well as banks Stanbic Bank and Bank of Africa and stole shs 10bn from over 1,500 sim cards.

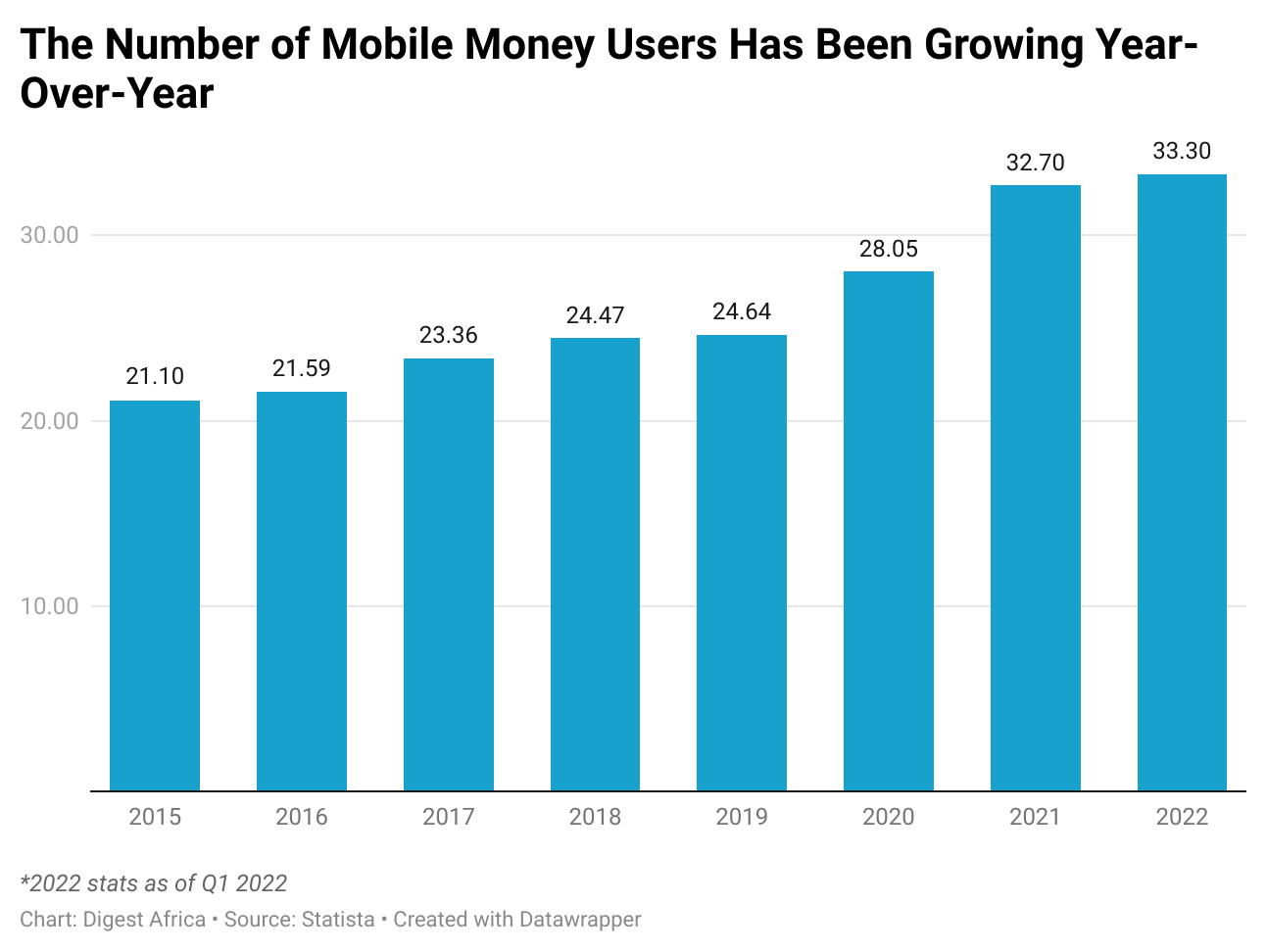

But these hacks have not slowed down mobile money adoption in Uganda. In fact, mobile money users have increased year-over-year, including in 2020 when a record 3.4m users joined Mobile money because of the COVID-19 restrictions that made cashless a viable option for the majority of Ugandans.

Uganda has adopted friendly Mobile Money regulations. In 2013, the Bank of Uganda issued the first mobile money guidelines. Under these guidelines, the Bank of Uganda would be responsible for the approval and supervision of mobile money services. At the same time, the Uganda Communications Council (UCC) would license and supervise the mobile network operators. But there were no concrete regulations outside of these guidelines,

All this changed in July 2020, when the National Payments Act (NPS) became law. The Act governed all operators of a payment system, payment service providers (PSP), and any issuer of a payment instrument.

The act gave power to the central bank to oversee all mobile money operations. It was also responsible for the licensing of all providers and for consumer protection. It also provided a regulatory sandbox framework that fintechs could join to test their services under the watchful eye of the central bank. This act also forced telcos, MTN, and Airtel to spin off their mobile money businesses into separate entities as a prerequisite to getting a license. This regulatory clarity, alongside a big unbanked population, has made Uganda an attractive market for fintechs.

So it is not surprising that the race to win the market attracted two well-funded competitors in SafeBoda and Wave Mobile Money to take on the incumbents, MTN Mobile Money and Airtel Money who have withered competitors like Orange Money and UTL’s M–Sente in the past to create a duopoly that might be hard to break.

Wave Mobile Money was started around 2018 in Senegal by Drew Durbin and Lincoln Quirk. These two started Sendwave as well in 2014, a remittance service. With Sendwave, anyone in Africa could receive money from North America and some European countries.

Sendwave was acquired by WorldRemit in a deal that was valued at $500m in 2020. But before this, Durbin and Quirk had been working on a product that eventually became Wave Mobile Money and piloted it in Senegal in 2018. After the acquisition of Sendwave, they turned their focus to Wave.

Since then, Wave has grown by leaps and bounds, especially in Senegal. It has between 4-5M users in Senegal making it the biggest mobile money service in the country, bigger than Orange Money: a service by Orange Telecom which is the biggest telecom company there.

Wave caused Africa-wide shockwaves in September last year when it raised $200m in the largest Series A ever on the continent according to TechCrunch. The list of backers was even more impressive: Founders Fund, Sequoia Heritage, Stripe, Partech Partners, and Ribbit Capital among others. This came at a valuation of $1.7bn making it one of the few African startups to achieve unicorn status and the first in Francophone Africa.

When Wave raised this money, it had already expanded to Ivory Coast looking to replicate its success in Senegal. Wave also expanded to Uganda, receiving regulatory sandbox approval in 2021.

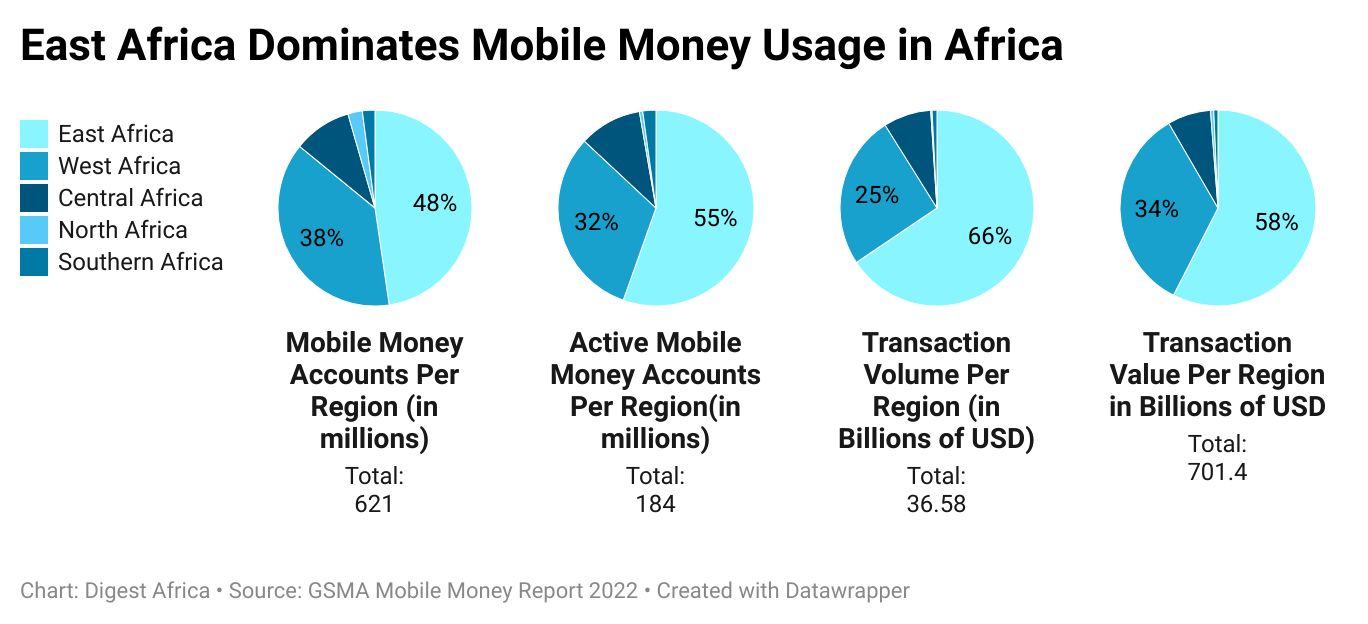

The true mobile money battlefield is Eastern Africa. Per the GSMA State of Mobile Money Report of 2022, there are 621m mobile money users in Africa. Of these, 48% are in Eastern Africa. The dominance increases when it comes to active users and transaction volume. East Africa accounts for 55% of the 184m active users in Africa and 65% of the $36.7bn worth of transaction volume.

In order to launch its operations in Uganda, Wave lured Nicholas Kamanzi as their country launcher. Kamanzi was one of the co-founders of Yoza back in 2015, before pivoting to a payments offering dubbed Yoza Pay in 2016. He was also the Fintech lead at Safeboda, presumably leading the development of the early Safeboda wallet and its fintech capabilities.

Apart from personnel, they do have interesting features as well. They are app-based, and not USSD-based like the incumbents. For users that don't have a smartphone, they provide a free QR card to transact with an agent. For a newbie in the market, Wave has built an impressive agent network. The users can also make free deposits and withdrawals and charge a 1% fee for sending money which is 70% cheaper than current Mobile Money services. In fact, this is Wave's biggest value proposition to users. Its charges are actually capped at UGX 12,500.

Wave aside, the other well-funded competitor is Safeboda. Safeboda started as a ride-hailing app but has since expanded to a host of services that include deliveries, e-commerce, and mobile money. Safeboda got its PSP license in January 2022 and has since gone on a marketing spree to convince its already existing users to start transacting on the app. Fintech services offered include bill payments, airtime, and data purchases on top of sending, withdrawing, and depositing money.

Can the two upstarts, usurp the incumbents?

It is highly unlikely that Safeboda or Wave can break the duopoly of MTN Mobile Money and Airtel Money. For starters, mobile money adoption on an individual level is built by a network effect that is, you join a network because you can transact with another person on that same network. This is where MTN Mobile Money and Airtel Money have an edge. In a country with over 35 million telephone subscribers, the majority of these users have MTN or Airtel sim cards, and in most cases, both. Also, sim cards acquired currently come with Airtel Money and MTN Mobile Money pre-registered. This essentially makes every new subscriber, a Mobile money subscriber for the telcos.

But also importantly, MTN and Airtel have built an agent network that covers the entire country. Actually, mobile money is a practical case of “banking the unbanked”, where millions of people have mobile money accounts without necessarily having bank accounts. The majority of these people are in rural areas. There are an estimated 14m bank accounts in Uganda, which is less than half of mobile money accounts. This is a sort of country-wide coverage that Wave and Safeboda will struggle to replicate. Also, the use of USSD codes is a big advantage that the telcos hold over the upstarts.

What is the likely outcome?

The emergence of Safeboda and Wave is a welcome competition, especially with their low fees. The reality is, both MTN and Airtel charge high fees for both withdrawals and sending money. The arrival of competition could force them to reduce these fees. In May 2021, MTN reduced its fees by 5.8% and if Wave and Safeboda continue making inroads in the market, then we can expect further reductions.

Safeboda will likely survive and could have the potential to become the third biggest Mobile Money provider in the country in the long term as it continues to convert its users into mobile money customers on its platform. And it can quickly have tens of thousands of agents by converting its riders/drivers into agents just like Yassir in Algeria. Currently, you can deposit using a driver as an agent, but you can't do withdrawals. Accepting withdrawals from the drivers and giving them the incentive to do so for example, a commission for the withdrawals could be a game-changer.

But the future looks bleak for Wave. It will require massive investment to get a foothold in the ecosystem. And even with such an investment, there are no guarantees of users down the road. Both MTN Mobile Money and Airtel Money can kill Wave by matching its fees. However, it is unlikely that the incumbents will do this. But Wave has struggled in the Ugandan market in 2022, laying off workers twice in a space of six months. Whereas layoffs are an industry-wide problem, and not specifically, Wave, this can show how its fortunes are tied to the amount of funding it can raise. Funding is highly influenced by external factors. This is a problem the incumbents don't worry about. Time, however, will tell.

Cover Photo/TechJaja

The writer is a retired founder, and now Editor-in-Chief at Digest Africa. You can reach him at +256771162922 or [email protected]

About us

Digest Africa is a leading provider of data and insights on investment into African startups that investors, corporations, researchers, banks, and startups can use to make meaningful decisions. We have a database encompassing;

- Over 1,400 venture capital deals for companies raising funding over the past 5 years

- More than 3,000 startup company profiles

- Over 400 investor profiles

Contact us for custom research and intelligence on the African startup ecosystem and venture capital. Email: [email protected]